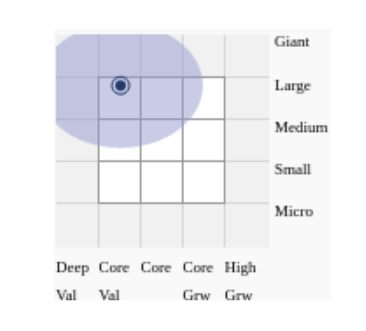

One of the major questions of the investing world is: “Value or growth?” I hear this question when I talk to people on the street and even when I read books by accomplished investors. In fact, Morningstar has codified this question into a popular infographic:

While this either/or question is popular, the dichotomy -- and the related logic it rests on -- always flummoxes me. At the core of the either/or question are two specific, orthogonal views of the world:

Value investing is the practice of investing in businesses which are selling at low price-to-book, price-to-sales, or price-to-cash-flow ratios or which have high dividend yields.

Growth investing is the practice of investing in businesses which have high book-value, sales, cash-flow, or earnings growth rates.

The definitions above are common, and the investment strategies they produce are convenient and widely practiced. Yet, if you look closely, this either/or thinking produces a number of paradoxes. For example, if you are a value investor, would you invest in a company, such as Sears, which spent many years on the path to bankruptcy, even though it was selling at a low price-to-sales ratio? Similarly, if you are a growth investor, would you invest in a company, such as Tesla, which is growing rapidly but is losing $1B/year?

Like the paradoxes of physics, the financial paradoxes above result from a flawed underlying theory. In this case, the flaw is in how you define value and growth investing. Simply stepping back and thinking about what your grandmother -- or Warren Buffet -- would tell you resolves the paradoxes.

“Price is what you pay. Value is what you get. ”

When purchasing a business, “what you get” are assets, debt, employees, and potential future business outcomes. Whether or not you got a good value depends on if the future value of the business ends up being more than what you paid for it. As such, good values can be had by businesses with negative growth (such as Warren Buffett’s purchase of Berkshire Hathaway), and terrible values can be had by businesses with great growth (such as the DotCom investor’s purchase of Microsoft). Peter Lynch elaborated on the latter scenario when he wrote:

“It’s a real tragedy when you buy a stock that’s overpriced, the company is a big success, and still you don’t make any money. ”

In the early days, while managing small sums of money, Buffett tended to purchase marginal businesses selling at favorable financial ratios, just as his mentor Benjamin Graham did. In time, Buffett’s partner, Charlie Munger, convinced Buffett to purchase higher-quality, growing businesses at less favorable financial ratios. In both cases, Buffett paid less than the businesses were worth. However, once Buffett began buying higher-quality, growing businesses at less favorable financial ratios, he could produce above-average returns on a portfolio much bigger than would have been possible using his old strategy. As you read how Buffett defines “value” and “growth” below, note that he thinks in terms of both/and, rather than in terms of a false dichotomy of either/or:

“But how, you will ask, does one decide what’s “attractive”? In answering this question, most analysts feel they must choose between two approaches customarily thought to be in opposition: “value” and “growth.” Indeed, many investment professionals see any mixing of the two terms as a form of intellectual cross-dressing.

We view that as fuzzy thinking (in which, it must be confessed, I myself engaged some years ago). In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive. ”

Next time you hear a discussion that hinges on a dichotomy of value vs. growth, remember this: all real investing is determining if what you are buying is worth more than what you are paying. Trying to divide the question (and your resulting investment decision) into value vs. growth simply leads to nonsense.

David R. “Chip” Kent IV, PhD

Portfolio Manager / General Partner

Cecropia Capital

Twitter: @chip_kent

Nothing contained in this article constitutes tax, legal or investment advice, nor does it constitute a solicitation or an offer to buy or sell any security or other financial instrument. Such offer may be made only by private placement memorandum or prospectus.